Population Bulletin Chapters

Introduction

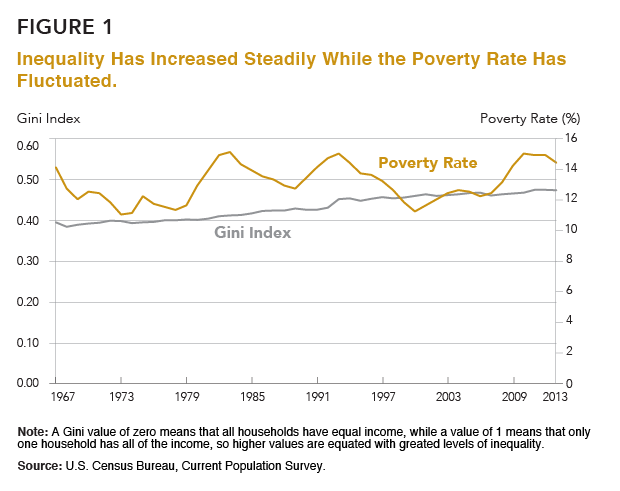

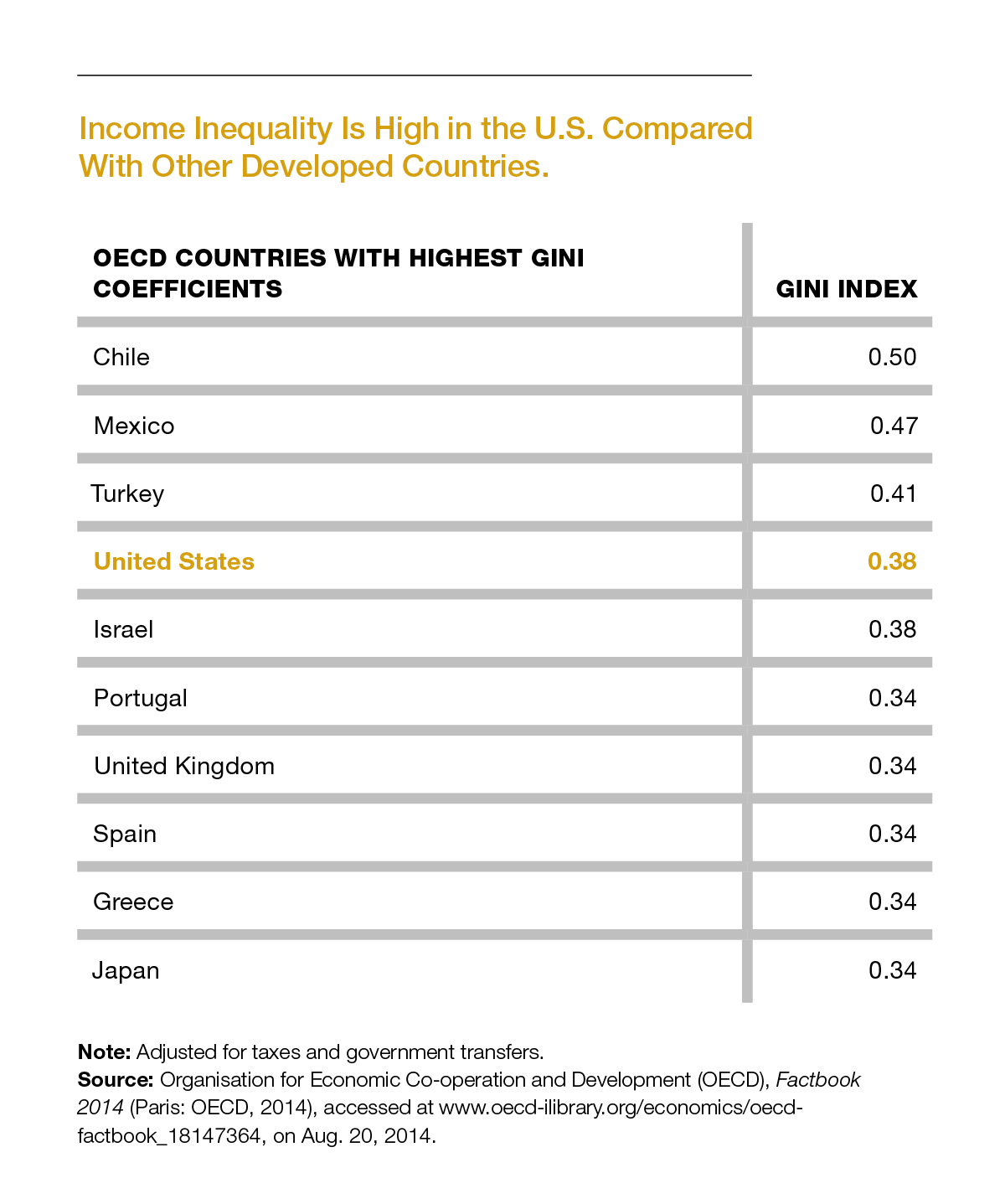

The Backdrop: Rising Inequality

Where Poverty and Inequality Intersect

The Generational Divide

Persistent Racial/Ethnic Gaps

Women Making Progress, But Gaps Remain

Education: The Great Equalizer?

Looking Ahead

">

">