Lillian Kilduff

Research Analyst

With the number of coronavirus infections surging, school districts across the United States are grappling with decisions about whether and how to re-open this fall. For online learning to be effective, students need access to computers and high-speed internet access, but a new analysis and interactive dashboard by PRB show sharp digital and economic divides among school-age children across states and between racial and ethnic groups.

In 2018, roughly 10% of U.S. children ages 5 to 17 did not have a computer—desktop, laptop, or tablet—at home, and 23% did not have home access to paid high-speed internet.1 Fully one-fourth of all school-age children were lacking either a computer or high-speed internet. Children without computers or high-speed internet at home were already at an educational disadvantage before the COVID-19 pandemic due to the growing need for students to access resources and submit assignments online. Many relied on computers and internet access at school or a local library to complete their work. As the pandemic prompted libraries to close and schools across the country shut down and moved to online instruction, this digital divide has become even more critical.

A racial and ethnic digital divide also persists. Half of all American Indian/Alaska Native children lack either computers or paid high-speed internet access (or both) at home (see Table 1). More than one-third of Black and Latinx children lack computers or high-speed internet at home, compared with only one-fifth of non-Hispanic white children and one in seven Asian/Native Hawaiian and Other Pacific Islander (NHOPI) children.

Economic barriers contribute to the digital divide between racial and ethnic groups. Poverty rates range from 10% among non-Hispanic white children ages 5 to 17 to 31% among Black children. American Indian/Alaska Native and Latinx children also have poverty rates far above the national average of 17%.

Black, American Indian/Alaska Native, and Latinx school-age children are two to three times more likely to live in households receiving Supplemental Nutrition Assistance Program (SNAP) benefits than white or Asian/Native Hawaiian and Other Pacific Islander children. Nearly 40% of Black and 35% of American Indian/Alaska Native school-age children live in households receiving SNAP benefits. Children whose households receive SNAP benefits are automatically eligible to receive free meals at school—which provide an essential source of daily nutrition for many of these children. With schools shut down, children of color whose families live in poverty and receive SNAP benefits are at much greater risk of going hungry and not receiving the nutrition they need during the pandemic.

Digital and Economic Divides of Children Ages 5 to 17 by Race and Ethnicity, 2018

| wdt_ID | Racial or Ethnic Group | Lacks Computer, High-Speed Internet Access, or Both | Family Income Below 100% of Poverty | Household Receives SNAP Benefits |

|---|---|---|---|---|

| 1 | American Indian/Alaska Native | 50 | 30 | 35 |

| 2 | Black | 36 | 31 | 39 |

| 3 | Hispanic or Latino | 34 | 25 | 28 |

| 4 | White | 20 | 10 | 12 |

| 5 | Asian/NHOPI | 14 | 11 | 11 |

| 6 | Two+ Races | 19 | 16 | 23 |

| 7 | All Children | 25 | 17 | 21 |

Nearly half (47%) of school-age children who live in poverty and 43% of those who receive SNAP benefits lack access to either computers or high-speed internet, compared with only 21% of children who do not receive SNAP benefits and whose family incomes are above the poverty line.

Within every racial and ethnic group, the share of school-age children without access to computers or high-speed internet is much higher for those who receive SNAP benefits and those who live in poverty (see Figure 1). While half of all American Indian/Alaska Native children lack access to computers and high-speed internet, this share jumps to 61% for those receiving SNAP benefits and nearly 70% among those living in poverty. Among non-Hispanic white children, the share without access to computers and high-speed internet nearly doubles from 20% to 39% for those receiving SNAP benefits and from 20% to 41% for those in poverty. Lower levels of economic well-being are widening racial and ethnic gaps in access to computers and high-speed internet.

Percent of Children Ages 5 to 17 in Different Racial/Ethnic Groups Lacking Access to Computers or High-Speed Internet by Poverty Status and Receipt of SNAP Benefits, 2018

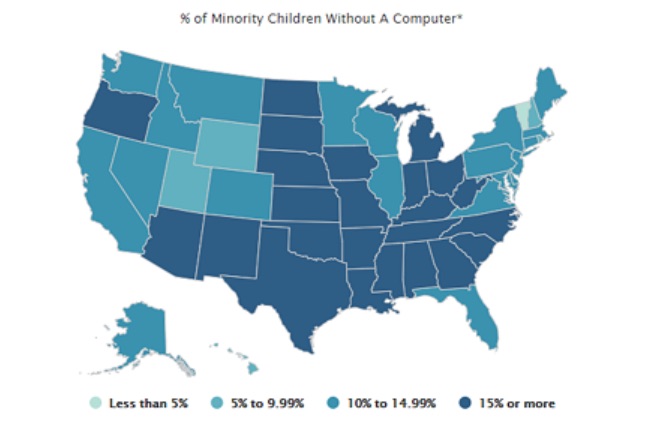

States vary widely in their shares of school-age children without access to computers and high-speed internet, from a low of 13% in New Hampshire to a high of 46% in Mississippi. In eight states—Alabama, Arkansas, Louisiana, Mississippi, New Mexico, Oklahoma, Tennessee, and Texas—more than 30% of children lack either or both computers and internet access, but this count rises to 31 states (including the District of Columbia) for minority children. More than half of school-age minority children in Mississippi, Arkansas, and South Dakota lack access to computers and high-speed internet at home.2

The economic divide is also present in every state. Twelve states (including the District of Columbia) have more than 20% of children ages 5 to 17 living in poverty, and 24 states (including the District of Columbia) have more than 20% of school-age children living in households receiving SNAP benefits. Concentration of poverty and SNAP receipt among school-age minority children is much higher than among non-minority children and is widespread across states. There are only 10 states where the share of minority children living in poverty drops below 20% and only three states (Utah, Vermont, and Wyoming) where the share in households receiving SNAP benefits falls below 20%. Conversely, nine states (Alabama, Arkansas, Louisiana, Mississippi, Ohio, South Carolina, South Dakota, Tennessee, and West Virginia) have one-third or more of minority school-age children living in poverty, and 22 states have more than one-third living in households receiving SNAP benefits.

Digital and economic divides among school-age children are linked to differences in reading and mathematics proficiency levels across states and between racial and ethnic groups. Proficiency in reading by the end of third grade is an important marker of overall educational development but, beginning in fourth grade, it is also essential for learning other subjects and keeping up academically.3 Children who reach fourth grade without being able to read proficiently are more likely to drop out of high school—reducing their earnings potential and chances for success.4 Similarly, proficiency in mathematics fundamentals makes college attendance and completion more likely, which increases earnings potential.5

In 2019, a shocking two-thirds of all fourth graders in the United States scored below the proficient level in reading, as did two-thirds of eighth graders in math. However, these shares are much higher among children in the racial and ethnic groups with the highest levels of poverty and receipt of SNAP benefits, and the least access to computers and high-speed internet (see Figure 2).

Reading and Math Proficiency of Children by Race and Ethnicity, 2019

Among Black and American Indian/Alaska Native students, at least 80% of fourth graders scored below the proficient level in reading, and 85% or more of eighth graders scored below the proficient level in math. More than three-quarters of Latinx fourth graders scored below the proficient level in reading and math in 2019. With higher levels of economic well-being and access to computers and high-speed internet, the shares of non-Hispanic white and Asian/Native Hawaiian and Other Pacific Islander children scoring below the proficient level in reading and math are much lower. These gaps in basic reading and math skills make it hard to envision how today’s children can become tomorrow’s productive workers in a globally competitive economy. In outlining his education policy in 2009, President Barack Obama argued that “The relative decline of American education is untenable for our economy, it’s unsustainable for our democracy, and it’s unacceptable for our children—and we cannot afford to let it continue.”6

States also vary widely in reading and math proficiency levels. For example, the share of fourth graders who scored below the proficient level in reading ranged from a low of 55% in Massachusetts to a high of 76% in New Mexico, while at least seven out of 10 children scored below proficient in reading in eight states. The share of eighth graders who scored below proficient in math ranged from a low of 53% in Massachusetts to a high of 79% in New Mexico, while at least seven out of 10 eighth graders scored below the proficient level in math in 17 states in 2019.

The low levels of proficiency in reading and math among children of color are even more concerning given the fact that minorities make up a growing share of the school-age population. The share of school-age children who are members of a racial or ethnic minority ranges from a low of 7% in Vermont to a high of 80% in the District of Columbia. Among minority students, only two states—Hawaii and Vermont—had fewer than seven out of 10 fourth graders who scored below the proficient level in reading. However, no states had fewer than seven out of 10 minority eighth graders who scored below proficient in math. For example, nearly half (48%) of school-age children in Louisiana belong to a racial or ethnic minority group, and 84% of minority fourth graders scored below proficient in reading while 88% of minority eighth graders scored below proficient in math. Taken together, roughly 40% of all fourth and eighth graders in Louisiana had already fallen behind academically even before the COVID-19 pandemic hit and schools closed.

As schools shut down in spring 2020, some districts like Los Angeles Unified tried to address the digital divide by distributing laptops to all students who needed them. In addition, some districts provided internet access to students without it by distributing hot spots or data plans. However, these solutions were not economically feasible in many districts serving low-income communities of color such as Prince George’s County Public Schools in Maryland. With 10 of the 15 largest school districts already deciding to begin the new school year online as of early August, reducing the digital divide and providing free and reduced-price meals for children who need them has become a daunting challenge across the country.

Unemployment rates remain at record highs, and with the supplemental $600 unemployment payments ending and Congress unable to agree on a new stimulus package, poverty levels and demand for SNAP benefits are both likely to rise this fall. A growing economic divide may further exacerbate the digital divide among school-age children, putting even more students at risk of falling further behind.

Loneliness makes us focus on ourselves but redirecting that focus outward… can change our outlook, our brains, and our body chemistry.

Steve Cole, Professor of medicine and biobehavioral sciences at the University of California, Los Angeles

Population Reference Bureau (PRB) is a core partner on the Population Council’s Evidence to End FGM/C: Research to Help Girls and Women Thrive—a UKAID-funded research consortium to help end female genital mutilation/cutting (FGM/C) within one generation. Our role is to build the consortium’s capacity for research utilization and develop innovative tools and products to improve how researchers communicate their findings about FGM/C to key decision makers.

A new PRB-prepared Evidence Brief, “Understanding Local Variation in How Female Genital Mutilation/Cutting Declines, Changes, or Persists: Analysis of Household Survey Data for Kenya, Nigeria, and Senegal,” summarizes the research consortium’s recent findings related to geographic differences in FGM/C trends among girls under age 15.

The researchers used advanced statistical modeling to show that FGM/C prevalence among girls tends to be concentrated in certain subregions and locations in Kenya, Nigeria, and Senegal—with local social norms driving the practice. Their findings underscore the importance of subnational policies in initiatives to end FGM/C and provide evidence for investing in community-level interventions that promote shifts in social norms, including religious norms.

The benefits of owning a home in the United States are well documented. Homes can create wealth for their owners that in turn can benefit families for generations. Homeownership can also reduce economic risk by protecting families from rising rent prices. Owning a home has also been associated with better psychological health and greater stability for homeowners’ children.1 Decennial census data can be used to monitor trends in homeownership and differences across geographic areas. The 2017 American Community Survey data provide a preview of patterns in the 2020 decennial housing data.

At the beginning of the 20th century, the homeownership rate, or the share of owner-occupied households, was 47 percent. That rate dropped to 44 percent in 1940 following the Great Depression, and then increased sharply between 1940 and 1950, from 44 percent to 55 percent. The post-World War II housing boom was fueled by low-interest loans for newly constructed homes, a provision of the G.I. Bill.2 The homeownership rate reached a peak in 2000 at 66 percent. Since the subprime mortgage crisis of 2007-2010, the rate has slowly declined, dropping to 64 percent by 2017.

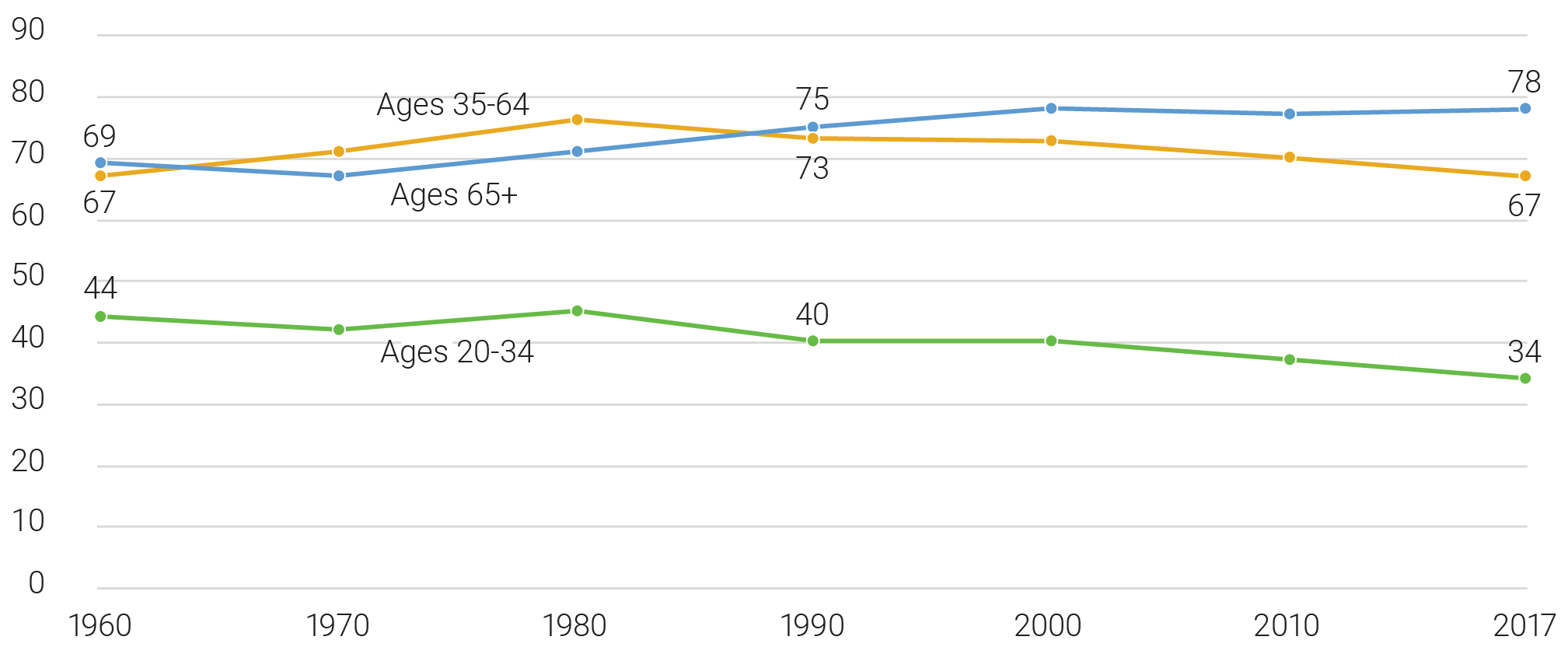

Most age groups experienced a decline in homeownership rates after the subprime mortgage crisis, which ended in 2010. Between 2010 and 2017, only adults ages 65 and older experienced an increase (1 percentage point), while the rates dropped for adults ages 20 to 34 and 35 to 64 (3 percentage points each) (see Figure 1). Historically, young adult householders (ages 20 to 34) have had lower homeownership rates compared with older householders (ages 65 and older), and the gap between these two groups has increased over time—from a 25 percentage-point difference in 1960 to a 44 percentage-point gap in 2017. For adults ages 35 to 64, the homeownership rate has returned to the same level it was nearly six decades ago (67 percent).

U.S. Homeownership Rate (%) by Age of Householder, 1960 to 2017

Source: Integrated Public Use Microdata Series (IPUMS), U.S. Census and American Community Survey: Version 8.0.

Between 1960 and 2017, the young adult homeownership rate dropped 10 percentage points, representing a shift from owning to renting. Although this trend suggests a change in housing preferences, more than two-thirds (67 percent) of renters report that they would buy a home if they had the financial resources to do so.3 The decline has also been linked to lower rates of marriage and household formation among young adults.4 The share of young adults ages 18 to 34 living with a spouse dropped from 26 percent in 2010 to 23 percent in 2017.

Homeownership rates also differ between urban and rural areas. In 2017, rural areas had a homeownership rate of 81 percent, compared with 60 percent in urban areas.5 This rural-urban gap is consistent across the country’s four regions but is widest in the Northeast, where the homeownership rate in rural areas (84 percent) was 26 percentage points higher than the rate in urban areas (58 percent).6 After each decennial census, the Census Bureau redefines urban and rural areas based on criteria related to population thresholds, density, distance and land use.7

Leading up to the late 1960s, various race-based housing practices, such as redlining (denying loans to people in certain neighborhoods) and mortgage discrimination, led to extremely high levels of black residential segregation and housing inequality.8 As part of the civil rights movement and following the death of Martin Luther King, Jr., Congress passed the Fair Housing Act of 1968. The act made it illegal to refuse to sell or rent to any person based on race, religion, national origin, or sex. Policymakers use data from the decennial census to enforce the act by examining rental and homeownership trends.

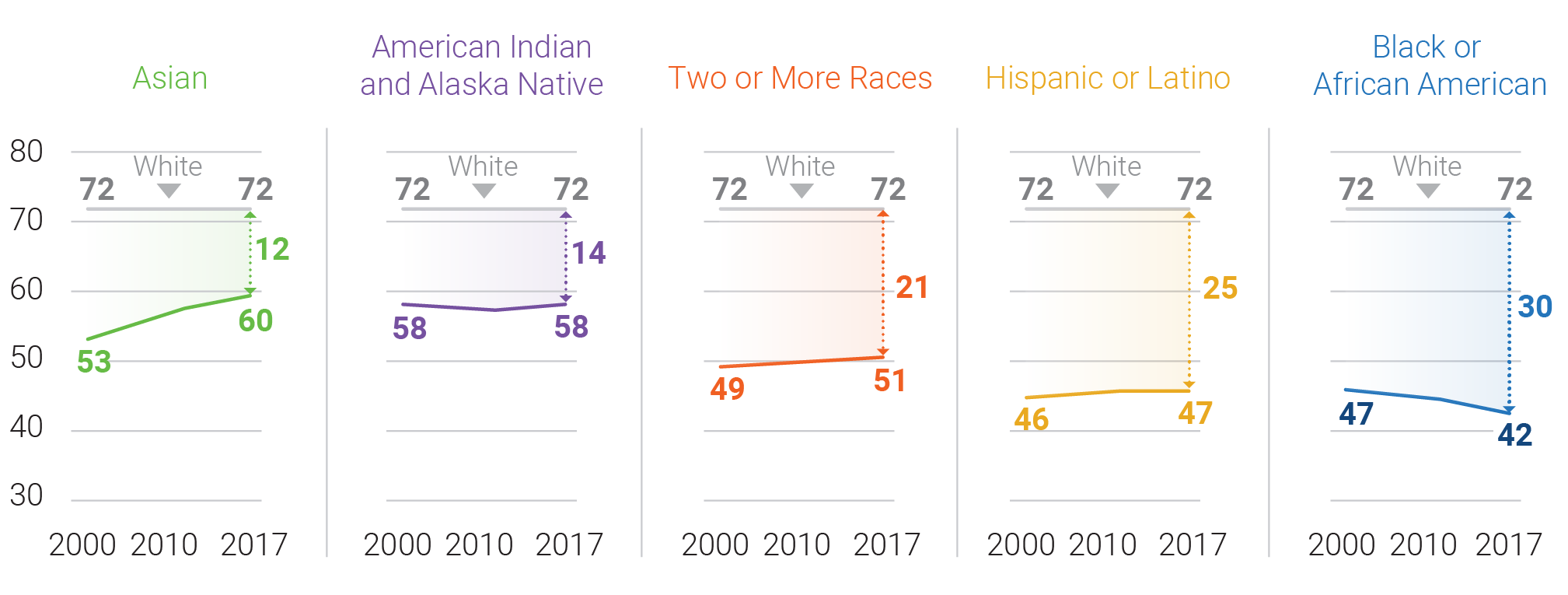

Despite these efforts, gaps in homeownership persist across different racial and ethnic groups. Historically, white householders have had the highest homeownership rates—a pattern that continues today9 (see Figure 2). In 2017, the white homeownership rate was 72 percent, compared with a national rate of 64 percent.

U.S. Homeownership Rate (%) by Race/Ethnicity of Householder, 2000 to 2017

Notes: “Other living arrangements” include householders living alone, with an unmarried partner, with other relatives, or with nonrelatives. Percentages may not sum to 100 due to rounding.

Source: U.S. Census Bureau, 2010 and 2017 American Community Survey PUMS.

Asian American and American Indian/Alaska Native householders had rates 12 and 14 percentage points lower than whites, respectively. The homeownership rate was lowest among black householders (42 percent—30 percentage points lower than the rate for whites). The size of the white-black gap in homeownership varies widely across geographic areas, with larger gaps in northeastern and midwestern cities and smaller gaps in cities in the South and West.10 Data from the 2020 Census will allow researchers to analyze homeownership rates at the region-, state-, county-, census tract-, and block group-level and ascertain whether the gaps between groups are shrinking or growing.

The overall homeownership rate dropped two percentage points between 2000 and 2017. This decline can be explained in part by changes in the racial and ethnic composition of householders. Whites have a high homeownership rate relative to other racial/ethnic groups, so as the white share of householders declined between 2000 and 2017, the homeownership rate also declined.

Recovery from the subprime mortgage crisis has been uneven. Both African American and American Indian/Alaska Native householders experienced declines in homeownership between 2000 and 2010. However, the American Indian/Alaska Native homeownership rate dropped just one percentage point between 2000 to 2010 and then rebounded by 2017, while the rate for African Americans continued to fall, declining 5 percentage points from 2000 to 2017. Predatory lenders targeted black and Latino communities prior to the mortgage crisis, resulting in high foreclosure rates when home values started to fall.11 Since 2010, homeownership rates for most racial/ethnic groups held steady or increased, but the rate for blacks continued to drop, especially among young adults. With higher incomes, white families are able to purchase homes an average of eight years earlier compared with black families, generating more equity and potential for growth in assets.12

The Asian American homeownership rate increased by nearly 7 percentage points between 2000 and 2017—more than any other group. The precise reasons behind this increase are unclear, but a high median income among Asian Americans, combined with a below-average homeownership rate, has positioned them for substantial gains in homeownership in the coming years.

This article is excerpted from Mark Mather et al., “What the 2020 Census Will Tell Us About a Changing America,” Population Bulletin 74, no. 1 (2019).

By 2030, young Africans are expected to make up 42 percent of the world’s youth and account for 75 percent of the those under age 35 in Africa. With such a large population of young people, supportive policies and programs on inclusive youth development are critical now more than ever. Harnessing the demographic dividend and expanding opportunities for young people—to the benefit of all Africans—will require sound data and evidence on the status of African youth.

Recognizing this need, the African Union Commission (AUC) has worked to build an evidence base of youth-specific data across a wide range of sectors to assist policymakers to make targeted investments and design effective interventions for young Africans. PRB has partnered with the AUC to create a policy brief focused on regional and continental findings on youth development in Africa to spark discussion among youth advocates and policymakers alike.

The policy brief examines inclusive youth development in Africa through the four pillars and enabling environment of the African Union Demographic Dividend (AUDD) Roadmap, which identifies key areas for increasing investments in youth, driving policy change, and setting member countries on a path towards a prosperous future. Using indicators selected and analyzed by teams of African youth researchers, the brief examines obstacles and opportunities facing African youth today. It calls for innovative, multisectoral approaches that holistically address youth experiences—across the employment, education, health, and governance sectors. The brief aims to make the case for evidence-based investments in young people and guide resource allocation across the continent.

Over the past decade, the incidence of conflict has been rising in sub-Saharan Africa (SSA), reversing a 20-year trend. Conflict’s pernicious effects on society are wide-ranging, even after stability returns, and extend to demographic trends. A body of previous research has found that fertility rates typically fall during conflict and rebound afterwards—but these effects are much smaller among less-educated women and in high-poverty settings.

A new PRB policy brief builds upon this previous research, breaking new ground by examining long-term trends in fertility in SSA among girls who lived in conflict zones when they were very young. The findings show that early childhood exposure to conflict has long-lasting repercussions—and those repercussions vary based on women’s eventual education.

Across 36 countries in SSA, girls who were exposed to conflict as children go on to have more children than peers who spent their childhood in stable environments, and they are also more likely to marry and begin childbearing before age 18. However, conflict-affected girls who attain secondary education have no increased likelihood of early marriage or childbearing. Education may offer girls affected by conflict a mechanism to build their resiliency and overcome some of the economic and social shocks of childhood in a conflict zone.

Population Reference Bureau (PRB) is a core partner on the Population Council-led Evidence to End FGM/C: Research to Help Girls and Women Thrive consortium—a UKAID-funded research program to help end female genital mutilation/cutting (FGM/C) within one generation. Our role is to build the consortium’s capacity for research utilization and to develop innovative tools and products to improve how researchers communicate their findings about FGM/C to key decisionmakers.

PRB has created a short video that shares key lessons from two studies in Egypt and Sudan that looked at effective elements of various social marketing campaigns. The video highlights how the four P’s—product, price, place, and promotion—can be used to design a high-quality FGM/C campaign. It also offers additional insights for program managers and designers that can help ensure social marketing campaigns to end FGM/C are grounded in the right principles and approaches. The video is based on the following two reports:

Older women face an important tradeoff between spending time with their retired husbands and continuing to work to increase their Social Security benefits and savings.

Nicole Maestas

">

">

">

">

">

">

">

">

">

">